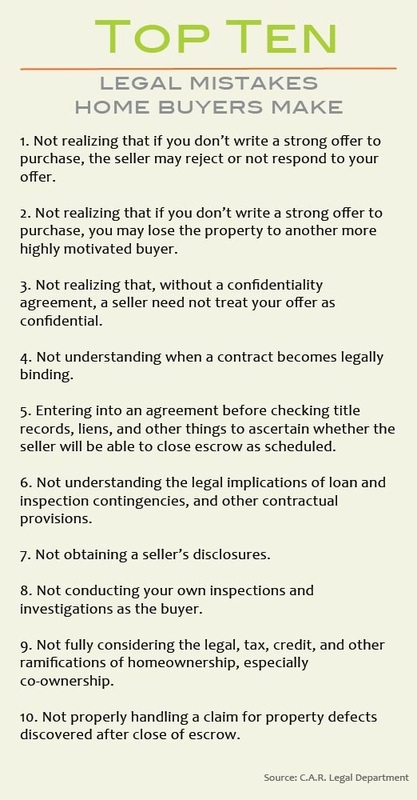

|

This guide is intended to provide the most common rental requirements across

the country. However, landlord-tenant laws change from time to time in every province. This guide is not intended to provide legal advice. If you require specific legal advice, contact your local rental authority or a lawyer. Rental issues can be similar in any area of the country, but authorities may treat them differently according to provincial or territorial legislation. For both landlord and tenant, it is important to understand your rights and responsibilities. Your rental agreement or lease should cover most rules and terms, but treatment of the rules and terms in your lease may vary depending on the province or territory of the rental property. Knowing the rules for where you rent currently is crucial because the legal statutes may differ from province to province. For example, determining when a landlord can enter residential premises with or without notice differs across the country. The types of dwellings that fall under provincial or territorial tenancy legislation also varies from province to province. For example, in some provinces mobile home park residents are protected under the provincial tenancy legislation, while in others they are excluded. Equipped with the right information, both landlords and tenants will be better prepared to deal with issues that might arise. CLICK HERE FOR RESIDENTIAL TENANCIES ACT It’s easy to overlook some of the things that can affect your budget and purchasing power when you’re considering a home, and one of the biggest factors that buyers overlook is the cost of their daily commute.

We’ve all heard that real estate is all about “location, location, location,” and properties in more desirable locations typically come with a higher price tag than similar properties that aren’t in a hot neighborhood. Yet the overall cost of living for choosing one location over another might be negligible when you factor in the commuting costs that are required—gas, vehicle maintenance, insurance—if you purchase a home that is significantly further from your workplace. If your mortgage is $200 less per month, but you’re spending an extra $200 in commuting costs, are you really saving money? Commuting costs aren’t just about the disposable income left in your bank account, either. It can even affect how much money you can borrow. If you’re a long-distance commuter, a loan officer may factor your travel costs into your debt-to-income ratio. Aside from how commuting affects your purchasing power or disposable income, there’s also the question of how it affects your quality of life—no one wants to spend hours a week just getting to and from work. The real estate market varies greatly from location to location, so the best way to get a complete picture of your purchasing power—and all the factors that go into your home budget—is to speak to a trusted real estate professional. Are you considering buying a Toronto property as a second home or investment? Perhaps you are looking for a small cottage or apartment where you can escape for vacation, or maybe you want to have another home closer to family. Maybe you want to rent out your second property and make a steady income from your investment. Whatever the reason, a second piece of real estate can be a fantastic investment. However, sometimes getting a mortgage on your second home can be a challenge.

Generally, a mortgage lender will have tougher standards for second home loans than primary home loans. This is because usually when you are buying a second home your finances will be stretched thinner and you will have less money to spare because you are already paying a mortgage on your primary home. This will mean that your second home mortgage can be harder to get and might have a higher interest rate. Here are some tips to keep in mind that will help you to get the best mortgage on your second property: Build up a decent amount of savings. Your mortgage lender will want to be able to see that you have a large amount of savings so that you will have enough to pay for the mortgage even if you were to lose your job. Pay off any credit card debt. Many lenders will be hesitant to approve your second home mortgage if they see that you have a lot of debt on your credit card. They will want to see that you have a low debt to income ratio so that you will be able to pay back the loan. Use the first mortgage as a good reference. If you have always made your payments on time and you are most of the way through paying off your first house, you could ask someone from your current mortgage company to vouch for you. The lender for your second mortgage will be reassured that you are a reliable person to loan money to. These are just a few tips to keep in mind in order to make getting a mortgage for your second property as easy as possible. To find out more about investing in Toronto property, contact me at [email protected] or phone me at 647-800-5201. Keyword: Toronto Property HST rebate rules don't include all your relativesThanks to www.buildersdirect.ca Thanks to buildersdirect.ca

What is a statement of adjustments? The Statement of Adjustments often catches many homebuyers off guard. Put simply, the Statement of Adjustments sets out any items that need to be added or subtracted from the purchase price, and shows the total amount of money that the purchaser will have to pay to the builder on closing day. The items that will be adjusted on closing are set out in the Agreement of Purchase and Sale. These items may be negotiable with the builder BEFORE the Agreement of Purchase and Sale is signed. Very rarely is the purchase price set out in the Agreement of Purchase and Sale the same amount that will be transferred on closing, as there are a number of items that need to be adjusted for, including: Deposit paid - A deposit on signing is standard practice in any real estate transaction, and can be a set amount ($500 used to be standard in St. John’s, but it is quickly increasing to $1,000) or a percentage of the purchase price. The purchaser gets to deduct this deposit off the purchase price, as it has already been paid. New construction extras and credits - When the home being bought is a new construction, it’s very common to see changes made to the materials used or the allowances for things such as flooring, light fixtures, cabinets, and so on, or changes to the floor plan and construction methods. These are all adjusted at closing as extras or credits. Taxes - Used residential housing isn’t generally subject to GST/HST in Canada, but new homes are. If the Agreement of Purchase and Sale doesn’t deal with this otherwise, the applicable tax will be added to the purchase price. However, it is quite common to see the agreed purchase price include all taxes, with the proviso that the purchaser assigns the GST/HST Rebate to the vendor. The details of how this rebate works are too boring to go into in this post. Rebates - In some transactions, the Vendor will rebate money to the purchaser for problems that arise after the agreement is signed. For example, if the sale is subject to a home inspection and the inspection reveals an electrical panel that needs replacing, the vendor and purchaser may negotiate a rebate to reflect the cost of fixing this problem, rather than having the panel actually replaced. Similarly, if damage occurs as the Vendor is moving out, there may be a rebate for repairs. Municipal taxes - In many cases, the homeowner has prepaid taxes to the end of the year or, in some cases, end of the month or quarter. The vendor is usually entitled to a credit for the portion of taxes that have been prepaid for the rest of the year. For example, if annual property taxes are $2,000 per year, and the house sale closes on October 1st, the vendor will get a credit of $500. The same goes for water taxes, if these are calculated separately and paid in advance. Oil or fuel adjustments - If the home has oil heating or propane tanks, the purchase price will usually be adjusted to reflect the value of fuel remaining in the tank. The tanks will be measured on closing day (or sometimes the day before), and the vendor will get a credit for the amount of fuel that is left. For example, if an oil tank is half full (or half empty!) on closing day, and the value of half a tank of oil is $450, this would be credited to the vendor. Rent and damage deposits - If the property is being used as a rental property and has tenants in place, the purchaser usually gets a prorated credit for the rent for the rest of the month. Similarly, if a damage deposit has been paid by the tenants, this whole amount gets transferred to the purchaser, as he or she will ultimately be responsible for returning in when the tenant eventually leaves. The physical deposit usually doesn’t change hands, it is just given as a credit towards the purchase price. The Statement of Adjustments is generally prepared by vendor’s lawyer well in advance of closing and sent to the purchaser’s lawyer for review. There may be some finagling of the numbers and negotiation between the two sides, but generally it’s pretty straightforward. The best advice is to review your Statement of Adjustments early and don’t be afraid to ask questions. And then ask them again! Closing Costs-thanks to RateHub

Closing costs, ranging from 1.5 to 4%1 of selling price, are the legal and administrative costs you will need to pay when your house closes. In addition to closing costs, there are other expenses and/or events that may require a cash outlay before, on or after your house closes. We will outline these in detail to ensure these often unexpected costs do not sneak up on you. Cash outlays required before your mortgage closes

On closing date, the following events will take place:

[1] Canada Mortgage and Housing Corporation (CMHC) |

WelcomePlease check our blog it will be updated periodically. Categories

All

|

RSS Feed

RSS Feed