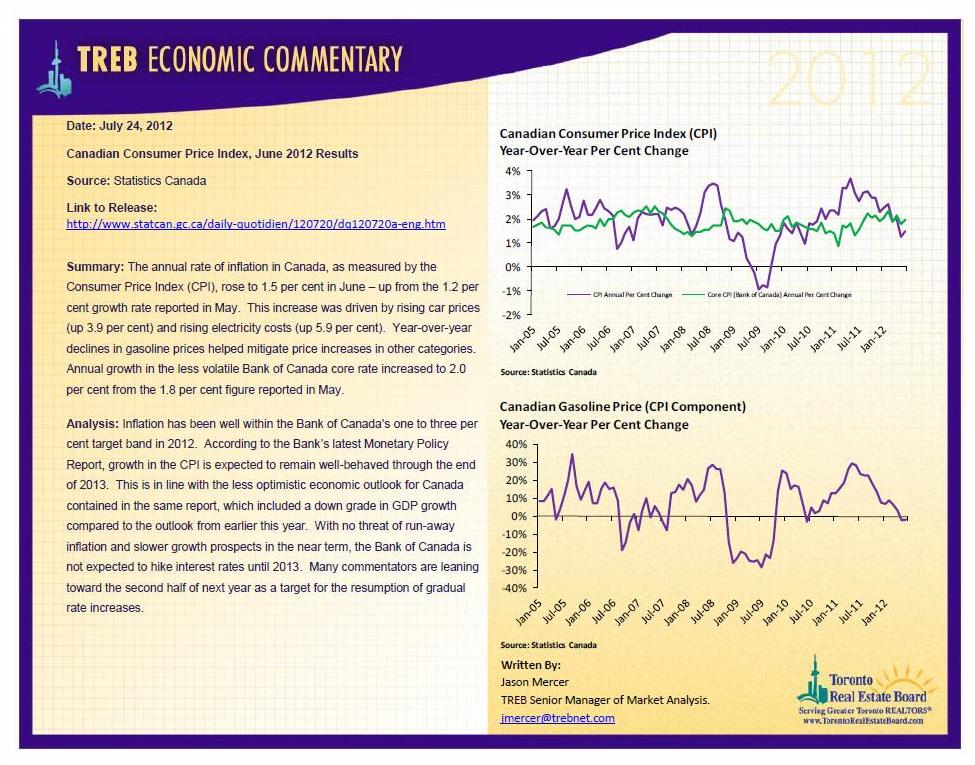

|

By Mark Weisleder

Many economists predicted a local real estate crash this year, with prices falling by up to 25 per cent. I didn’t see that prediction coming true and it didn’t. Nor will do I believe it will happen in 2013. Here’s why: 1. Homes are more affordable In 1990, the average GTA home cost half of what it does today. But interest rates were 12 per cent for a five-year term at the time. So if a two- bedroom condo cost $250,000 in 1990 and you had a 20-per-cent down payment, your monthly carrying costs, including interest, taxes and common expenses, were about $2,500. The average rental for a two-bedroom condo at the time was $1,100, according to the Housing New Canadians research group. So the economics of ownership made no sense. Today, even with a price of $500,000, if you have a 20-per-cent down payment, with current interest rates at 3 per cent, the total monthly payment is what it was in 1990. It is still $2,500 per month, including common expenses and taxes. But in downtown Toronto, the average rent paid for a two-bedroom unit is now close to $2,500 per month. Most tenants who can afford $2,500 a month or more in rent can probably afford to buy a home now, if they have 10 per cent down payment or more. 2. The lesson from 2012 Toronto Real Estate Board statistics up until Nov. 30 show 82,200 units had sold in the GTA so far this year. In 2011, it was 84,900, and in 2010 it was 81,900. The average price on Nov. 30 was 2 per cent higher than a year ago. If anything, the market has remained very stable for the past three years. 3. Impact of mortgage rule changes is minor The mortgage rule changes imposed in early July lowered the amortization period to 25 years if you were putting less than 20 per cent down and lowered the percentage of your income that could be used for borrowing from 44 per cent to 39 per cent. The result was that buyers who would have purchased in late summer or fall moved up their purchasing decision to the spring. By fall, this meant many would-be first-time buyers were looking to rent instead of buy. This contributed to low vacancy rates. 4. 2013 will be fine Despite the doom and gloom, Toronto condo rental vacancy rates are 1.7 per cent. This means that for those people who cannot sell their condos, there are plenty of renters who can cover the monthly costs. 5. Debt-to-income ratio not relevant As our American friends like to say, “that dog won’t hunt.” Every month we are told that because the ratio of household debt to household income continues to rise — and is now at 164 per cent — there is a danger of a real estate collapse. What this really means is that the average Canadian household has an income of $100,000 and total debt of $164,000 (of which their real estate debt constitutes-two thirds). Again, as stated earlier, with interest rates at 3 per cent, this is not a dangerous problem. If interest rates were 12 per cent, as they were in 1990, or if all your debt was on your credit cards (with interest rates averaging 18 per cent), then this would be a serious problem. Note to readers: pay down or eliminate your credit card debt in 2013. Note to government: with mortgage interest rates at 3 per cent, it is almost criminal for lenders to be able to charge 18 per cent on consumer credit cards. 6. Interest rates may not rise until 2015 The U.S. Federal Reserve is now saying it won’t raise rates until 2015. Our rates can’t differ much from theirs without harming our economy with a strong dollar and slower growth. These are all things to keep in mind in the coming year. Somebody has been predicting a Canadian real estate market collapse for the past 12 years. It hasn’t happened yet and won’t happen in 2013. More columns by Mark Weisleder Mark Weisleder is a Toronto real estate lawyer. Contact him at [email protected]  Mortgage insurance is a protection tool for lenders against the possibility of mortgage default. The need for mortgage insurance typically comes into play when home buyers make a down payment between 5% and 20% of the purchase price of their home.

This insurance by no means protects the buyer and is intended to be a protective tool for the lender. To obtain such security, lenders are required to pay an insurance premium which they will pass onto the buyer. This premium is equal to a percentage of the home purchase price financed by the mortgage, then either added to the mortgage or presented as a single lump-sum to be paid off by the home buyer. Mortgage insurance is usually between 0.5 and 2.9 per cent of the total mortgage amount. Where the percentage sits on the spectrum is dependent on the down payment. The higher the down payment, the lower the mortgage insurance rate. As a result, it is imperative that you ensure you are balancing between how much you can afford as your down payment and how much insurance you are willing to commit to. The Requirements The primary factor that makes a mortgage insurance required is if a buyer is not able to get up to 20% of the home purchase price as down payment. This automatically makes mortgage insurance a requirement. In general, to qualify for mortgage insurance, you need to have the following requirements:

Benefits to the Buyer Many Canadian’s don’t even qualify for a mortgage anymore. To qualify, they will have to save an additional $25,000 which will take them another 3 1/2 years. Managing to come up with a 20% downpayment is totally out of the question. What mortgage insurance allows is the possibility of making a down payment of as little as 5% and getting ownership of a significant capital asset, rather than never owning a home. Also, it is possible to put the mortgage insurance with the mortgage payments over the life of the mortgage. It is easier to manage and while home buyers will be paying more, they now have a major capital asset with them. CMHC Mortgage Loan Insurance The CMHC is one of Canada’s leaders in housing and mortgage services. They provide a range of tools such as calculators and flexible financing options to help first time home buyers and investors with the purchase of a property and the finances that revolve around that purchase. The CMHC provides mortgage loan insurance to those who qualify among other services. Additionally, they offer an incentive which allows home buyers to reduce their mortgage loan insurance. By purchasing an energy-efficient home or by opting-in to do energy-saving renovations, the CMHC Green Home flexible financing option makes home buyers eligible for a 10% mortgage insurance premium refund in addition to an extended amortization without a premium surcharge. Combining the benefit of a low down payment with the CMHC Green Home flexible financing option not only lets you have little financial outflow but also gives you an incentive to live greener, which could have other benefits, including energy savings and reduction of utilities. Other Ways to Save You can further reduce the mortgage insurance through two means. The first is by paying off your mortgage sooner. By reducing the overall length of your mortgage, you are reducing the number of payments for your insurance premium. Overall, we are seeing Canadian’s paying off their mortgage faster. RateHub’s analysis of the Canadian mortgage market shows that Canadian’s are paying off their mortgage five year’s sooner, observed between the years of 2008 and 2012. Additionally, being financially stable also helps. Income validation is a major factor that affects how much insurance premium you pay. An analysis put together by Canadian Living shows that an individual with a full-time job would pay a $9,000 premium after putting $50,000 down on a $500,000 house – a 10% down payment. The premium works out to be $21,375 for an individual making the same down payment as a self-employed buyer. Conclusion By opting-in to pay mortgage insurance on a potential purchase, first time home buyers open many doors, the biggest being the ability to pay as little as 5% down towards the purchase of a new home. On top of that, various financial incentives such as the CMHC’s Green Home flexible financing option allows home buyers to capitalize on the lower down payment, live a greener & cost effective lifestyle and be able to save money in the process.  Three of the biggest demographics buying condos in Toronto are retirees, immigrants, and first time home buyers, all are looking to purchase brand new units. According to a new report by Genworth Canada, the demand for condos is increasing, which will likely lead to an increase in prices within the upcoming year. Experts at Genoworth project a price hike of 2.5 percent to $312,352 which is quite significant.

Toronto’s population has increased by more than 17 percent since the last census period 2006 and over a 100,000 new residents are moving into our city yearly. Many within this group are used to living in urban settings, the 905 composition simply does not satisfy their needs. Affordability is also key because condos remain the most affordable option to purchase in Toronto taking up just over 35 percent of a median household income Condo Prices Grow at Moderate Pace in Q2

July 18, 2012-- Greater Toronto REALTORS® reported 6,435 condominium apartment transactions during the second quarter of 2012 – down by 2.6 per cent compared to 6,609 transactions reported in the second quarter of 2011. New listings for condominium apartments were up substantially on a year-over-year basis, climbing by 19 per cent in comparison to 2011. “The condominium apartment market has been the best-supplied market segment in the GTA this year. Many condominium projects have completed over the past year and this has resulted in a substantial increase in listings and ultimately more choice for buyers,” said Toronto Real Estate Board President Ann Hannah. “The greater degree of choice in the condo market translated into a moderate rate of price growth compared to what was experienced in the low-rise market segment.” The average price for second quarter condominium apartment sales was $342,212, representing a 3.2 per cent increase over the same period in 2011. “Sellers seemed to be well-aware of condo market conditions in the second quarter. On average, units were priced in line with buyer expectations, with apartments selling for 98 per cent of the asking price in less than a month’s time,” said Jason Mercer, TREB’s Senior Manager of Market Analysis. 6,435 6,609 Second Quarter 2012 Second Quarter 2011 Click here to see Full Report Greater Toronto Realtors reported 3,679 sales through the first 14 days of July 2012, representing a 5.6 per cent increase compared to the 3,484 sales reported for the same period in 2011. New listings were up by 14.4 per cent over the same time frame. “Housing demand remained strong in the first half of July. Sales growth occurred in the regions surrounding the City of Toronto. In the City of Toronto, where sales were down, the relatively higher cost of home ownership likely prompted some buyers to purchase elsewhere in the GTA. Higher costs in the City of Toronto include the upfront payment of the additional land transfer tax,” said Toronto Real Estate Board (TREB) President Ann Hannah.

The average selling price in the first half of July was $473,466 – up by 2.3 per cent compared to last year. On average, homes sold for 98 per cent of the asking price in 25 days – in line with July 2011. Price growth was strongest in the City of Toronto, climbing by 3.5 per cent to $496,645. “A better supplied market contributed to a slower annual rate of price growth in July relative to the first half of 2012,” said Jason Mercer, TREB’s Senior Manager of Market Analysis. “As buyers benefit from more choice in the second half of this year, expect price growth to slow to a more sustainable pace.” |

WelcomePlease check our blog it will be updated periodically. Categories

All

|

RSS Feed

RSS Feed