Moving into a new home is an exciting time, and you're probably daydreaming about decor and paint schemes and new furniture. But before you get into the fun stuff, there are some basics you should cover first.

Change the locks Even if you're promised that new locks have been installed in your home, you can never be too careful. It's worth the money to have the peace of mind that comes with knowing that no one else has the keys to your home. Changing the locks can be a DIY project, or you can call in a locksmith for a little extra money. Steam clean the carpets It's good to get a fresh start with your floors before you start decorating. The previous owners may have had pets, young children, or just some plain old clumsiness. Take the time to steam clean the carpets so that your floors are free of stains and allergens. It's pretty easy and affordable to rent a steam cleaner-your local grocery store may have them available. Call an exterminator Prior to move-in, you probably haven't spent enough time in the house to get a view of any pests that may be lurking. Call an exterminator to take care of any mice, insects, and other critters that may be hiding in your home. Clean out the kitchen If the previous occupants wanted to skip on some of their cleaning duties when they moved out, the kitchen is where they probably cut corners. Wipe down the inside of cabinets, clean out the refrigerator, clean the oven, and clean in the nooks and crannies underneath the appliances. Barrie teacher Cheryl O’Keefe doesn’t know how she would have survived the stress-induced sleepless nights of July had school not been out for the summer.

O’Keefe is among Toronto region home buyers and sellers who got caught in the spring real estate downturn. When the sale on her house finally closed a month past the originally agreed-upon date, it was the end of an expensive nightmare for O’Keefe. Others who sold their homes in this year’s once frenzied real estate market, are still struggling to complete their transactions. Lawyers, realtors and mortgage brokers report a surge in calls from distressed sellers whose buyers purchased in the heat of the market, only to find that the subsequent drop in the home’s value is more than the cost of walking away from a deposit. Others, who bought unconditionally, have discovered they can’t get the financing to meet their purchase obligation. In some cases, the bank appraisal has come in at a value below what a purchaser agreed to pay, leaving the buyer scrambling to make up the difference. O’Keefe’s real estate agent, Peggy Hill of Keller Williams, says closings have been stalling since the end of June. Barrie home prices may not be as high as some closer to the city, but the drop has been precipitous. “Our average price for a home in Barrie is $471,822 for July. In March it was $570,199. We’re talking about a $100,000 difference,” she said. That is still $40,000 above the average price of July 2016. But back then, 208 of the 260 homes listed sold. “This July we have 201 sales so the sales are still there but with 683 active (listings),” said Hill. “That’s the real picture.” The GTA-wide picture is similar. When the regional market peaked in April, the average home price — including every category from condos to detached houses — was $919,449. By July, it had fallen to $746,216, although prices were still up 5 per cent year over year. There were 9,989 sales among 11,346 active listings in July of 2016, according to the Toronto Real Estate Board. This July, listings soared to 18,751 listings, with only 5,921 sales. O’Keefe had lived in her bungalow for only about two years when she decided to sell it in February, about the time property prices were peaking. Her basement apartment was standing empty and she wanted to downsize. The real estate frenzy in Barrie mimicked Toronto’s and most of the 43 showings of O’Keefe’s house were, in fact, people from Toronto. Like many homes at the time, O’Keefe’s sold in about a week for more than the listed price. The buyer put down a $25,000 deposit and requested a longer-than-usual four-month closing date of June 28. “That was fine. It just gave me more time to do what I had to do,” said O’Keefe. What she had to do was find a new home for herself in the same fiercely competitive market. She lost a couple of bidding wars and turned her back on a century home she loved because she knew it would go at a price she could never justify. When she happened on an open house that fit her needs, O’Keefe bought it with a May 28 closing — a month ahead of when her own home sale was to be finalized. She arranged bridge financing to cover both mortgages for that month. It all looked good on paper. But as the spring wore on, O’Keefe grew uneasy. The buyers of her house had not requested the usual pre-closing visit. Usually, excited new owners want a look around. O’Keefe got her realtor to call. No response. A week from closing, she had still heard nothing. At 4:50 p.m. on closing day, her lawyer talked to the purchaser, who admitted he was having difficulty with the closing. By then, O’Keefe had been living in her new place a month and was paying two mortgages. She agreed to extend the closing to July 14. When that didn’t happen, O’Keefe agreed to a second extension to July 31. The date came and went. Finally on Aug. 2, her lawyer called to say the buyer closed. “Every step of the way everything that could be a headache has been a headache,” she said. O’Keefe’s realtor says that so far, in her office, even problematic closings have been finalized. But some have been disappointing. “There have been deals where we’ve had to take less commission. The seller had to take less money to make it close because at that point they’re euchred. “It’s usually $40,000 to $50,000 because of our price point. In other areas I know it’s in hundreds of thousands of dollars,” said Hill, referring to areas such as Richmond Hill, Newmarket and Aurora, also hard hit by the market’s downward slope. Some buyers have requested extensions on new home purchases because their old places didn’t sell, said Hill. “That’s understandable,” she said. “In March, you wouldn’t dare go in with an offer conditional on the sale of a home. The problem is, in April, when all hell broke loose, everybody started putting their houses on the market fearing they had missed the top.” Many have arranged bridge financing and moved on. But others haven’t been as fortunate, said Toronto lawyer Neal Roth. He has been getting about five calls a week since mid-May from home sellers struggling to close on transactions. “There is this horrendous domino effect going on where people in the spring were rushing into the market for a variety of reasons, committing to prices that in some instances were well beyond their means,” he said. Most of his callers represent one of two scenarios. First, there’s someone paid $1.5 million for a house that has since become worth $1.4 million, so they want to get out of the purchase. “The other type of person says, ‘The bank promised me 60 per cent financing. Now that I’m at $1.5 million I should still get the same 60 per cent, not realizing that you have to come up with the 40 per cent of your own cash, or that the bank said 60 per cent when you were at $1.2 million, not $1.5 million,” said Roth. While he thinks some sellers got greedy and some buyers should have been more careful, he hasn’t encountered anyone who got caught playing the property market. “They’re all average people. None of them have been speculators as far as I know,” he said. It’s not uncommon for mortgage brokers to hear from home buyers struggling with financing, said Nick L’Ecuyer of The Mortgage Wellness Group in Barrie “But what we’re getting now is people who are in sheer turmoil. They don’t know what to do at all,” he said. Some sellers, who planned to use their equity to put down 20 per cent or more on another home, don’t realize they can’t get bridge financing from a bank if they don’t have a firm purchase agreement on their old house. Then there’s the hard truth that the house they’re selling isn’t likely to go for as much as they expected earlier in the year. They can put down just 5 per cent and apply for a government-insured mortgage, but that’s more complicated and costly, said L’Ecuyer. The Appraisal Institute of Canada doesn’t have statistics on the number of lender-commissioned appraisals that come in short of the agreed-upon price of a home. But based on anecdotal accounts, it’s happening more now in the GTA, said institute CEO Keith Lancastle. “Any time you go into a situation where you make an abrupt change from a seller’s market to a buyer’s market — where you see a slowdown for whatever reason — you can encounter this situation,” he said. The role of an appraiser is to provide an unbiased opinion of a property’s value at a given point of time. “A heated market does not automatically translate into a true market value. When you take away the heat, all of a sudden it settles down into something that is perhaps more reflective of what true market value is,” said Lancastle. He says he’s still surprised by how emotional what is routinely now a million-dollar home buying experience can be. “It’s arguable that mortgage lending should not be underwriting that emotion and that notion of a sober second thought is really important, not only for the purchaser, but also for the lender,” he said. Buyers tempted to walk away from a deposit need to realize that they may still face a lawsuit, says L’Ecuyer. If you bought a house for $500,000 and decided to forfeit the deposit, and the seller gets only $450,000 from another buyer, you can be sued for the difference, he said. There is also the possibility of being sued by a realtor who isn’t getting a commission, and for additional legal and carrying costs. Roth said there are people who don’t even realize that when they back out of a sale, their deposit is automatically lost. O’Keefe believes that because she priced her home on the low side, it hasn’t lost any value. “You start talking to people and this is happening to so many,” she said. “I’m lucky that my house closed.” Condo prices in Canada’s two most expensive housing markets have climbed rapidly over the past year, making it harder for millennials to complete their first purchase.

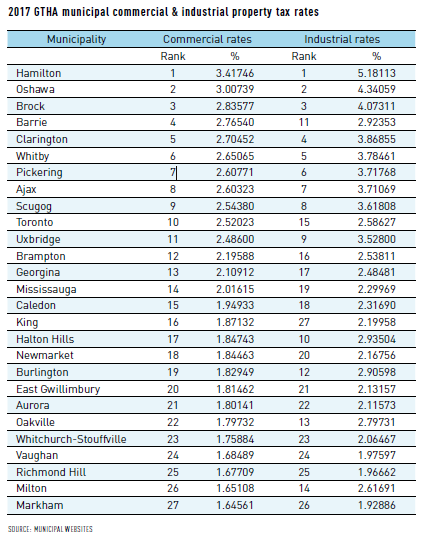

The average price of Greater Vancouver condos sold in July reached a record $664,944, up 15.9 per cent from a year earlier. In the Greater Toronto Area (GTA), the average price of condos sold last month hit $501,750, up 23.2 per cent from July, 2016, although down 7.3 per cent from the peak of $541,392 in April. Millennials – people born between the early 1980s and early 2000s – are struggling to save for adequate down payments to enter the housing market in Canada, especially in the Vancouver and Toronto regions. Real estate firm Royal LePage focused on a subset dubbed “peak millennials,” who now range in age from 25 to 30. “Facing challenges their baby-boomer parents never encountered, peak millennials are confronted with significant obstacles that vary depending on where they live,” Royal LePage chief executive officer Phil Soper said in statement. In a survey of 1,000 peak millennials across Canada, 64 per cent of the respondents said they believe properties in their respective regions are unaffordable. The survey’s respondents in British Columbia had the most pessimistic view of their ability to purchase, with 83 per cent of those canvassed in B.C. saying their area is unaffordable – the highest rate in the country. Leger conducted the online survey in June for Royal LePage, citing a margin of error of plus or minus three percentage points, 19 times out of 20. Fifty-three per cent of the respondents nationally said they are willing to spend up to $350,000 for their home purchase. Thirty-five per cent of those surveyed said they already own a home while 50 per cent stated that they rent. Most of remaining 15 per cent said they live with their parents or family members. “The pent-up demand for housing from millennials is enormous, with only a third of this large demographic currently owning a property and an overwhelming majority desiring to be homeowners,” Mr. Soper said. In the GTA, $350,000 would be enough to acquire a “starter” condo with 910 square feet of living space, compared with the same budget in Fredericton landing a four-bedroom detached house with 2,568 square feet in the New Brunswick capital, according to Royal LePage. Nationally, 61 per cent of the peak millennials surveyed said they are willing to move to another city or suburb to find more affordable housing. Commercial and industrial property tax rates decreased in almost every GTHA municipality in 2017, when compared to 2016 rates. Commercial rates dropped, on average, about 0.03 per cent, while industrial fell 0.09 per cent. Hamilton continues to have the highest overall business tax rates in the GTHA, while Markham continues to have the lowest. Across the region, municipalities decreased their industrial tax rates over 2016 rates, with Oshawa having the greatest decrease at 0.26231 per cent. The only municipality to raise both its commercial and industrial rates was King, which increased its commercial rate by 0.03 per cent, and its industrial rate by 0.04 per cent.  Purchasing a Home Post DivorceIf you have recently gone through a divorce and are considering buying a home, there are some things that you need to consider before you start scanning real estate listings.

Divorce is challenging both emotionally and financially and can leave you in a position drastically different than the one you were in before or during your marriage. Buying a home is a considerable investment, so it is important to cover all the bases before you commit to anything. The following tips can help you clarify your situation and your options, ensuring that you make a sound decision when you buy a home after a divorce. Tips For Buying After A Divorce1. Take some time after the divorce.Divorce is considered one of the most stressful events a person can go through. While you may be feeling compelled to purchase a home and move on with your life, you should be aware that if you have recently gone through a divorce, you may not be thinking as clearly as you imagine. If you are like most people, buying a home will be one of (if not the) largest financial decisions you make. Major financial decisions like this are best made with a cool head, something that may be impossible for you to manage for a while. Making sound decisions is something discussed extensively in selling a home while going through a divorce. Far too many people make hasty choices because they have not thought things through clearly enough. From the seller perspective, one of the parties often wants to keep the marital home at all costs even though it does not make sense financially. There is nothing wrong with renting for a six-month or year lease to let the dust settle after your divorce. After some months have passed, you will have a better idea of what your financial situation is and what you want your life to look like moving forward – both of which play a major part in the home buying process. 2. Get clear on your financial situation post-divorce.One of the biggest considerations when buying a home is your financial circumstances – what income you are bringing in and what your ongoing costs are. These factors limit your ability to make a down payment and to pay a mortgage. But, while your finances may have been relatively consistent before the divorce, there is a good chance that the divorce is going to cause some disturbances. Depending on where you’re at, you may need to pay attorney fees, child support, spousal support, divide up savings and investments, etc. You may have considerably less money after the divorce than you did before, or more financial obligations – like taking care of children on your own. See these tax tips for divorcing couples which show some of the considerations post-divorces when it comes to finances, taxes and living arrangements. You want to look carefully at the divorce documents to verify what your obligations are following the divorce. Your lender will want to check that you can afford a mortgage, so you will need to have all your documentation in order. 3. Make sure to separate your finances. Save It ‘s okay to share expenses in a marriage, so you probably have a lot of mutual obligations with your ex. Separating your finances is part of the divorce process, but sometimes there can still be accounts and obligations that slip through the cracks. The easiest way to find problem areas is to order your credit report. You can get your report for free once a year, but even if you are not entitled to a free report, it is still worth paying the fee to get accurate information on your finances. Separating your finances may be difficult – and may even require talking to an attorney – but it is worthwhile. You want your credit score to reflect your financial situation accurately, and avoid having it negatively impacted by the actions of your ex after your divorce. Getting a mortgage after divorce often is challenging. One thing to make certain of before buying a home after a divorce is the removal of your name from the mortgage of the marital home. Sometimes divorcing couples hold off on getting one of the spouse’s names removed from the mortgage and deed. Not being removed from a mortgage could be any number of reasons including the current housing market condition or the financial situation with your spouse. Getting your name off the mortgage, however, is a critical step moving forward to the next chapter of your life. Keep in mind that a divorced person’s credit rating can be impacted by still being part owner of the marital home. Being on the marital mortgage can lead to not being qualified for a new mortgage loan, due to the high level of overall debt load still showing up on your credit report. 4. Work on your credit score.If you get your credit report and find that you have a great credit score, congratulations! Unfortunately, many people find that their score is worse than they expected after they have divorced. You may have been a non-wage earner in the marriage, taking care of the home and the kids. Or maybe you only needed to work a part-time job because your spouse was successful. Even if you were earning enough money, if your spouse was reckless with credit, you may still be stuck with a bad score. Post-divorce, it will be necessary to check your credit score to make sure you were not dragged into a rough spot due to your partner’s bad financial habits. Luckily, you can raise your score. The higher you can get your score, the better rates you can get on a mortgage, which can save you tens of thousands of dollars in the long run. If you have a low score, do some research and find out ways to boost it. It will take time, but it is usually worth it if you want to buy a home. Take time to understand the different mortgage programs that will best serve your needs. If you can get to a twenty percent down payment will be critical to eliminate paying private mortgage insurance. A fee that is solely for the lender and does nothing for you as a homeowner. 5. Choose a location you will love. Save If you are in a position where you can buy a home after your divorce, choosing a location can be one of the harder decisions to make. This could be one of the most important consideration when buying a home after a divorce. How close do you want to be to your ex? Do you have children that you want to be relatively close to their parent? The closer you are to your ex, the more likely you are to wind up running into one another when you are out. You may be okay with such meetings, or you may want to avoid them at all costs. Talking to your Realtor about your concerns is a good idea before you start shopping. He or she can point you to areas that will fit your specific needs. Was your former home in a more secluded area and you think that a neighborhood may be better if you have kids? Make sure you reflect on how to pick a neighborhood that will be suitable for your new living style post-divorce. Do you need to be thinking about school districts? These are all crucial location decision that should be given serious thought. 6. Select a property that fits your lifestyle – condo vs. home.If you just got divorced, you are well aware that your life is different now. Before you start house hunting, take some time to brainstorm about what kind of life you want to have moving forward, and what kind of home will facilitate that life. Make a list of what you want your new home to be, and talk to your agent about your list to make sure he or she is directing you toward the right kind of options. One of the first considerations should be whether you want a condo or a house. Have a look at the pros and cons of both housing choices to get an understanding of what may be best in your current situation. Is it better to have a home for the kids with a yard for them to play in? Do you travel a lot for your work or have long hours that makes owning a home more challenging? Maybe a condo would be a better option given that most of the exterior will be taken care of for you? These are the kind of questions you should be asking yourself. Maybe buying a home or condo is not the right move at all. Could renting be a better option? 7. Work With a Realtor That Has Divorce Experience.The real estate agent you choose to work with is important under any circumstances. When you are going to be buying a home and have just gone through a divorce, it can be even more important. Choosing a Realtor who understands divorce can be helpful from both emotional and financial circumstances. The real estate agent should, in fact, have gone over many of the items mentioned above if they an excellent agent. 8. Find a Great Mortgage BrokerChoosing a mortgage broker you are comfortable with is almost as important as selecting a real estate agent. You want someone who understands your financial situation well enough to place you in the best loan for your individual circumstances. Work with someone you trust who will work hard to get you the best terms and mortgage rate. Before you go out looking for homes, make sure you have a pre-approved loan. Getting a pre-approval puts you in a position to buy a home, something a good listing agent will surely be looking for when considering any offers. Be sure you understand the difference between a pre-approval and a pre-qualification which is significant! Linked here is a copy of CREA’s submission on Guideline B-20 Residential Mortgage Insurance Underwriting Practices and Procedures.

CREA remains concerned that changes to housing finance rules are being driven by the realities of specific geographic markets and may have collateral damage to the balance of the housing market. Potentially introducing additional tightening measures while the housing market is still absorbing numerous government imposed changes over the last several years puts affordability at risk and could imbalance many local markets. We encourage boards and associations to participate in the public consultation to share your comments in support of the real estate industry. The deadline for submission is Thursday, August 17, 2017. |

WelcomePlease check our blog it will be updated periodically. Categories

All

|

RSS Feed

RSS Feed

{kind=link}

{kind=link}